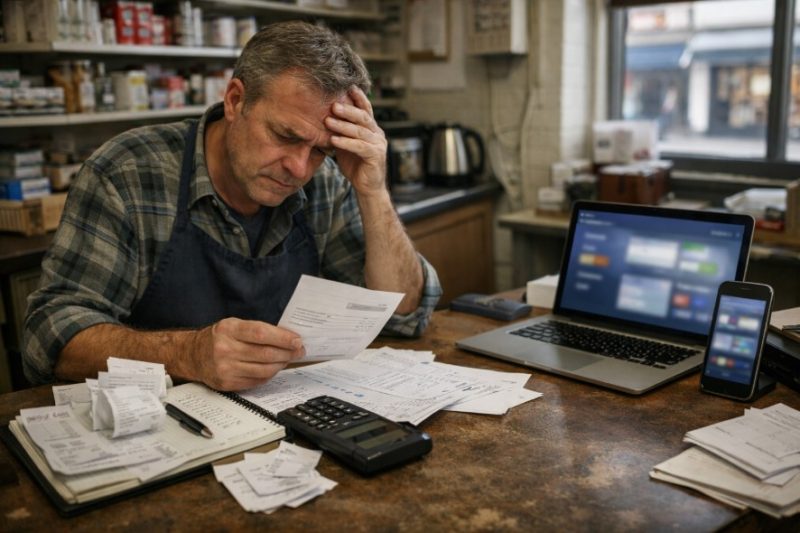

Cash flow is the lifeblood of any small business, yet many UK owners are still relying on slow, manual payment processes that drain both time and money.

While consumer payment habits have shifted dramatically, business infrastructure has struggled to keep pace. The gap between what technology offers and what most SMEs actually use is growing wider by the year.

The irony is stark. Customers are ready and willing to pay quickly. It’s the back-end systems catching up that remain the problem.

Why Are UK Small Businesses Are Underusing Digital Payout Tools Despite Faster Payment Solutions?

Sectors Already Leading on Payout Speed

Retail and ecommerce have pushed furthest ahead when it comes to real-time payout infrastructure. Tools like Stripe and Zettle now offer instant or near-instant settlement, reducing manual reconciliation and minimising the friction that leads to abandoned transactions. These aren’t enterprise-level solutions, they’re accessible to small operators too.

Interestingly, the online gaming industry offers one of the clearest examples of how payout speed and transparency can be built directly into a platform’s infrastructure.

Platforms operating in the online casino space have made rapid, verifiable payouts a baseline expectation for users (source: https://www.gamblinginsider.com/uk/best-payout-online-casinos). That same expectation, speed, clarity, reliability, is now being demanded across every transactional sector.

The Cash Flow Cost of Slow Payouts

Late payments continue to be one of the most damaging issues facing UK small businesses. A 2025 Coface survey found that 90% of UK businesses are dealing with payment delays from customers, a figure significantly higher than comparable economies like France and Germany. That level of exposure doesn’t just affect day-to-day operations; it actively blocks investment in better systems.

The cost compounds over time. Businesses stuck waiting on invoices can’t reinvest in stock, staffing, or growth. When the tools exist to dramatically shorten payment cycles, continuing to rely on manual processes isn’t just inefficient, it’s expensive.

What Small Businesses Should Adopt Now?

Consumer adoption of digital payment methods is already well ahead of where most SMEs are operating. According to UK Finance data, 57% of UK adults are registered for at least one mobile wallet service, with 87% of those making at least one transaction per month. Businesses that can’t accept these payment types are effectively turning customers away.

Beyond point-of-sale upgrades, the case for broader digital financial tooling is equally compelling. Research from Starling Bank found that SMEs using digital tools for financial tasks report an average 41% time saving over manual processes, with the potential to add £25.3 billion to the UK economy. That’s not a marginal improvement, it’s a structural shift in how productively businesses can operate.

The Real Price of Delaying Digital Payments

Setup complexity and card processing fees are the most commonly cited barriers to adoption. But these concerns, while valid, often mask the larger cost of inaction. Every week spent managing payments manually is a week of unnecessary admin, delayed reconciliation, and lost time that could be spent on growth.

The businesses pulling ahead aren’t necessarily the ones with the biggest budgets. They’re the ones that made early decisions to prioritise payment infrastructure, treating fast, transparent payouts not as a luxury, but as a basic operational requirement. For UK small businesses still on the fence, that window for easy adoption won’t stay open indefinitely.